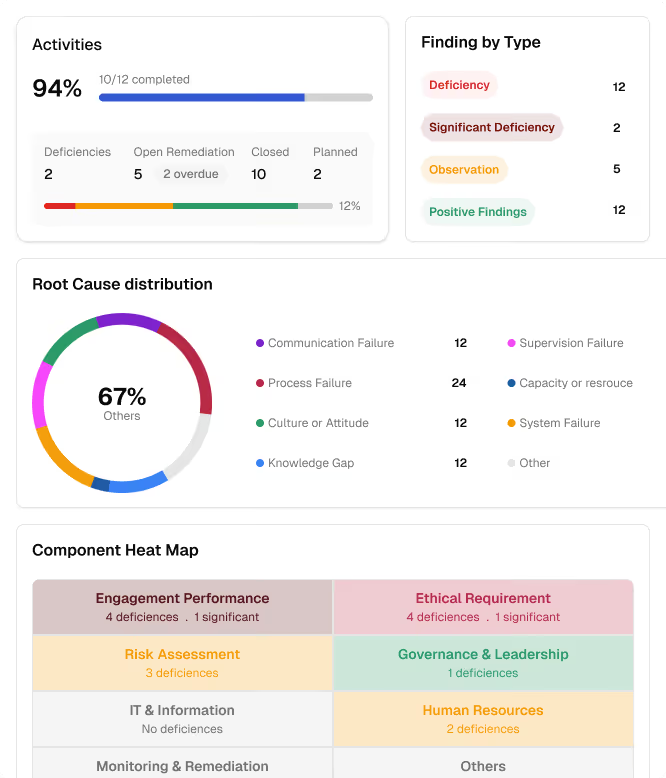

TL;DR

AI audit software can be compliant with professional audit standards—but only when it supports human judgment, documents methodology, preserves evidence integrity, and aligns with frameworks such as ISA, PCAOB, and ISQM 1. Compliance is not automatic; it depends on how the tool is configured, governed, and used within the engagement.

Why Compliance Is the First Question Auditors Ask

When firms evaluate AI audit software, the conversation quickly moves beyond features to standards alignment. Regulators and inspection bodies do not audit the algorithm—they audit whether the engagement team obtained sufficient appropriate audit evidence and maintained professional skepticism. That means any AI-assisted workflow must map cleanly to established requirements for planning, risk assessment, documentation, and review.

What “Compliant” Actually Means for AI Tools

| Dimension | What auditors should expect | Why it matters |

|---|---|---|

| Human judgment and accountability | AI suggests; auditors decide. Alerts are hypotheses, not conclusions. | Standards require human evaluation of evidence and risk. |

| Methodology transparency | Documented rules, models, thresholds, and data transformations. | Reviewers must be able to reperform or evaluate the approach. |

| Evidence traceability and audit trail | Immutable logs, version history, and traceable outputs. | Workpapers must support conclusions years later. |

| Data governance and security | Access controls, encryption, retention, and client confidentiality. | Ethical and legal obligations extend to AI pipelines. |

| Explainability and defensibility | Clear reasons why a transaction or pattern was flagged. | Black-box outputs are hard to defend in inspection. |

Mapping AI Workflows to Major Audit Standards

| Standard / Framework | Relevant requirement | How compliant AI software supports it |

|---|---|---|

| ISA 315 / PCAOB AS 2110 | Risk assessment and understanding the entity | Population analytics, trend views, and anomaly heat maps inform risk scoping. |

| ISA 500 / PCAOB AS 1105 | Audit evidence—relevance and reliability | Data lineage, reconciliation checks, and exportable workpaper artifacts. |

| ISA 230 | Audit documentation | Timestamped runs, parameter logs, reviewer notes, and conclusion fields. |

| ISQM 1 | System of quality management | Firm-wide policies for AI use, training, monitoring, and technology governance. |

| IESBA / AICPA ethics codes | Ethics, confidentiality, competence | Secure processing, role-based access, and documented competence for AI-assisted procedures. |

A Practical Compliance Checklist for Firms

| Control area | Pass criteria | Common gap |

|---|---|---|

| Data reliability | Source, scope, and totals documented and reconciled. | Using client-prepared exports without reliability testing. |

| Model and rules governance | Version control and change logs for rules/models. | Silent model updates between planning and fieldwork. |

| Documentation quality | Each conclusion tied to assertion and materiality. | Screenshots without narrative or conclusion. |

| Security and confidentiality | Encryption, access logs, and data retention policy. | Processing client data in unapproved environments. |

Where AI Audit Software Adds Compliant Value

When governed properly, AI audit platforms help firms meet standards more effectively by enabling:

- Full-population testing: Analyze complete datasets instead of relying only on sample-based coverage.

- Consistent control execution: Apply the same rules, thresholds, and review logic across engagements.

- Faster risk triage: Prioritize high-risk exceptions for human review and escalation.

- Defensible documentation: Preserve run logs, reviewer notes, and conclusion trails in workpapers.

- Improved engagement oversight: Give reviewers clear dashboards for status, findings, and remediation tracking.

Red Flags That Signal Non-Compliance Risk

Not every AI audit product is inspection-ready. Watch for these warning signs:

- Alerts treated as final conclusions: Teams accept flags without testing relevance, reliability, or context.

- No reproducible audit trail: Runs cannot be recreated with the same data, parameters, and outputs.

- Opaque model behavior: The system cannot explain why items were flagged or scored as high risk.

- Weak governance controls: No version logs, approval workflow, or change-control process for rules/models.

- Data handling gaps: Unclear retention, access logging, encryption, or residency controls for client data.

Final Thoughts

AI audit software is not inherently compliant or non-compliant—it is a tool whose compliance depends on design, deployment, and oversight. Firms that treat AI as an extension of professional judgment—with clear methodology, defensible documentation, and robust governance—can align AI-assisted audit work with the standards clients and regulators expect.

Conclusion

AI audit software can meet professional audit standards when it preserves human judgment, documents methodology, maintains evidence integrity, and supports quality management requirements. Evaluate vendors against a practical compliance checklist, map workflows to ISA, PCAOB, and ISQM 1 expectations, and govern AI use as part of the firm’s overall system of quality management.